November 2024 Market Summary

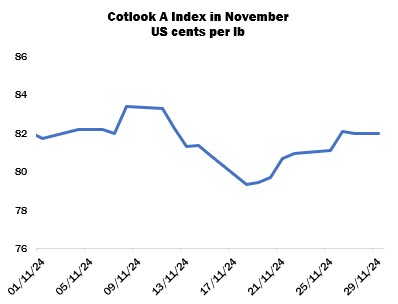

International cotton prices, as measured by the Cotlook A Index, stood at 82.05 cents per lb on November 29, marking a decline of just five points from the end of the previous month. In New York, the March contract closed 10 points higher than at the end of October, as a bearish trend in the middle of the period was reversed, with modestly higher settlements in eight of the last nine sessions under review. The lead contract’s high point for the month was 73.43 cents per lb, on November 7, while the low proved to be 68.91 on the fifteenth.

Import demand was encouraged by the retreat of futures back below the 70-cent mark and was subsequently dampened by the upward reversal of prices. Mills in several markets, notably Bangladesh and Vietnam, were in need of cotton to cover nearby gaps in their requirements, resulting from long-standing hand-to-mouth buying, and exacerbated by difficulties associated with opening Letters of Credit and making timely payments in the former country. Therefore, spinners in those destinations sought customary supplies, available nearby or afloat when possible. Buyers in Pakistan and Turkey also secured foreign growths, but business was price sensitive.

Robust buying was reported at or in parallel with the Cotton USA summit in California, confirmed by US export reports following the conference that included two consecutive marketing-year high net additions to upland export registrations (318,500 and 324,100 running bales). Pakistan, Vietnam and Turkey featured as the top buyers in both reports, while China recorded more modest quantities. In addition to business in US cotton, it was understood that an even greater volume of Brazilian changed hands during the same period. However, logistical problems and delayed shipments continued to be reported in Brazil. Exports in the first three weeks of November were some way behind the pace set in the previous month at 157,000 tonnes.

Later in the month under review, delegates attended the 7th Mediterranean Cotton Roads conference in Izmir, Turkey, where modest quantities of cotton sales were reported, perhaps a reflection of firmer futures levels during that period as well as the less urgent need for spinners to procure supplies following volume business in the preceding weeks. Greek and Brazilian lots found buyers, while Turkish supplies encountered less interest on price grounds.

Meanwhile, the lead contract on China’s Zhengzhou cotton futures platform closed the month barely altered at 14,010 yuan per tonne. Ginning of the 2024/25 crop in Xinjiang progressed rapidly, reaching over four million tonnes by the end of November. Estimates of the final output increased in view of very good yields: the China Cotton Association raised its figure to 6.35 million tonnes and Cotton Outlook’s forecast was placed at 6.5 million. Some observers anticipate an even higher total, and our figure may be subject to further revisions as ginning approaches a conclusion.

In the United States, the Department of Agriculture made a marginal reduction to its domestic production figure in its November supply and demand report, to 4.19 million 480-lb bales. The impact of Hurricane Helene on the Georgia crop was perhaps less severe than expected, or was offset by higher yields elsewhere, and so the estimate for that state was raised by 200,000 tonnes, while decreases were recorded for Texas and others. The Department also lowered its figures for global production, consumption, trade, and beginning stocks, with the result that world ending stocks were placed at 75.75 million bales, down from 76.33 million last month.

The last USDA crop progress report for the season indicated that harvesting was 84 percent complete beltwide by November 24, ahead of the same moment last year and the 80 percent five-year average. Growers thus began to assess planting options for the upcoming season.

Picking was complete in Pakistan by the end of the month. According to the Cotton Ginners’ Association, seed cotton arrivals totalled almost 5.2 million bales by November 30. Local observers indicated that quality parameters had declined and higher grades were therefore in tighter hands, while discounts were available for poorer qualities. In India, arrivals were robust during the month in view as picking expanded. The Cotton Corporation of India placed arrivals at 4.7 million bales by the end of November. The Corporation meanwhile procured supplies in defence of the Minimum Support Price (MSP), and also sold stocks through its daily e-auctions.

In the Southern Hemisphere, sowing was in its final stages in Australia and most young stands were developing well, but stormy weather was received over much of the growing belt early in the month. ABARES forecasts lint production in 2024/25 at one million tonnes, representing a seven percent decline on the previous year. Early planting began to expand in Bahia, Brazil under favourable conditions while preparations for sowing of the first crop (safra) were underway in Mato Grosso. Ginning of the 2024 crop was all but complete. The official forecasting agency, CONAB, increased its estimate of cotton output to 3.7 million tonnes, still modestly below the figures put forward by the producers’ association ABRAPA and the exporters’ association ANEA (3.97 and 3.85 million, respectively). Planting intentions increased in Argentina and progress advanced to perhaps 60 percent complete.

In November, Cotton Outlook raised its forecast of global raw cotton production in 2024/25 by 204,000 tonnes to 25.5 million. The adjustment was a result of increases for China, the US, the African Franc Zone and Pakistan, partially offset by reductions for smaller producing countries. For consumption, our estimate was raised by 120,000 tonnes to 24.5 million, attributed to higher figures for Bangladesh, Vietnam and Pakistan, while reductions were recorded for India and Brazil. World stocks at the end of the current season are therefore expected to rise by 1,020,000 tonnes, up from the 936,000-tonne increase put forward a month ago.

Smaller adjustments were made for 2023/24, with the result that the margin by which production is estimated to have exceeded consumption in that campaign has been reduced slightly, to 874,000 tonnes.