May 2024 Market Summary

Volatility characterised New York futures during May, but the spot month ended the period little changed on balance. The July contract closed at 76.15 cents per lb, representing a net decrease of 228 cent points. The inverted July/December spread remained relatively narrow compared to recent levels, placed on May 31 at 104 cent points. Certified stocks meanwhile declined overall, particularly following the decertification of just over 60,000 bales on May 29.

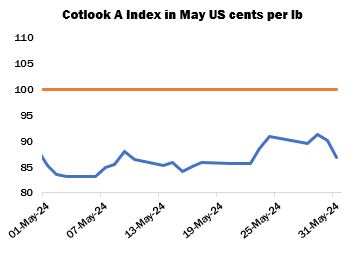

International cotton prices, as measured by the Cotlook A Index, closed the month at 86.80 cents per lb, representing a modest loss from the end of April, of 150 cent points.

The physical market was relatively subdued during May, as buyers’ and sellers’ price ideas became more difficult to reconcile and downstream demand showed few signs of a marked recovery. Some desirable qualities were also in short supply, for example US, West African and Australian higher grades (particularly following the wet weather last month that raised concerns regarding the quality composition of the last-mentioned crop). Nonetheless, enquiry from mills continued and pockets of business, typically in small quantities to cover spinners’ nearby requirements, were concluded. Bangladesh and Pakistan were mentioned in this regard, despite persisting issues in both countries accessing Letters of Credit, while India sought a range of import supplies, including various African origins and Australian.

In China, Zhengzhou cotton futures declined by 430 yuan on the month, closing at 15,270 yuan per tonne. International cotton prices therefore maintained a competitive advantage vis-à-vis local supplies, so import demand continued. Enquiry was in evidence for higher grades from Brazil and Australia, for example, but the specific qualities desired were at times difficult to supply and negotiate at workable prices. Meanwhile, it is thought that some business was concluded in the confines of the China Cotton Industry Development Summit that took place at the end of May in Xi’an, with Brazilian 2024 crop prominent.

According to USDA export reports covering May, China accounted for almost 432,000 running bales (60 percent of the total to all destinations) of new net sales registrations of upland cotton in the current season. Shipments to that destination totalled just over 278,000 bales, while net new sales for 2024/25 amounted to just 15,400 bales.

In the United States, planting approached 60 percent complete by May 26, slightly ahead of recent averages, and 60 percent of the crop was said to be in a ‘good to excellent’ condition by the same date. Squaring had begun in some parts. Weather conditions were mixed across the cotton belt during the month in view. West Texas received welcome precipitation, followed by above-average temperatures. In the Memphis Territory, water stood in fields following excessive rains. Some non-irrigated fields across the belt, however, remained too dry.

The Department of Agriculture’s May WASDE report included the first detailed projections for the 2024/25 marketing year. US production is forecast at 16 million bales (480 lbs), the figure advanced at the Outlook Forum in February. Domestic consumption is estimated at 1.9 million and exports at 13 million bales. As a result, the season’s ending stocks are placed at 3.7 million bales, versus the season’s beginning stock of 2.4 million, the second lowest of the 21st century.

Heatwave conditions persisted in the latter half of the month in Pakistan, delaying planting and raising concerns of heat stress on seedlings and young plants. By May 24, planting progress in Punjab had reached 75 percent of the target area, around 22 percent behind the same point last year. Some resowing was expected, but the earliest planted cotton matured well in the heat and small quantities of arrivals had been reported.

Sowing of the Indian new crop, meanwhile, was behind schedule in the Northern Zone, also as a result of high temperatures. Private estimates suggest that around 50/55 percent of the expected total area had been planted there by the end of the month. The Meteorological Department updated its long-range forecast for this year’s Monsoon season, a key factor for the country’s cotton output. It indicated that rainfall is likely to be above the long period average, at 106 percent, and maximum and minimum temperatures are expected to be higher than normal for most of the country during June.

In Brazil, CONAB once again increased its official production forecast, to 3.64 million tonnes, further increasing the margin by which the previous record output would be exceeded. Concerns, however, lingered among observers regarding the potential effects of rainfall in April on the crop in certain areas. Harvesting meanwhile expanded gradually in Argentina, to around 30 percent complete by the end of May. Rainfall improved soil moisture levels, but then delayed field work and may have affected quality in some parts. In Australia, clearer conditions had assisted harvest activities for a period, but unhelpful wet weather shortly returned, heralding a scarcity of uncommitted high-grade cotton. The Australian Cotton Shippers Association stated that picking was around 35 percent complete by the middle of the month.

Cotton Outlook’s global raw cotton output estimate for 2023/24 was increased by 307,000 tonnes in May, attributed largely to India, Pakistan and Brazil. The forecast for 2024/25 has also been raised, by 67,000 tonnes, owing to upward adjustments for India, Uzbekistan and others, while reductions were made to the figure for Pakistan and some smaller producing countries. For consumption, our estimates for 2023/24 and 2024/25 were reduced, by 79,000 and 126,000 tonnes, respectively. Declines in Pakistan account for most of the change in both seasons, partially offset by small upward adjustments elsewhere. World ending stocks in 2023/24 are therefore expected to rise by 979,000 tonnes, up from 593,000 at the end of April, while an increase of 622,000 tonnes is anticipated in the following season (compared with 429,000 a month ago).