January 2025 Market Summary

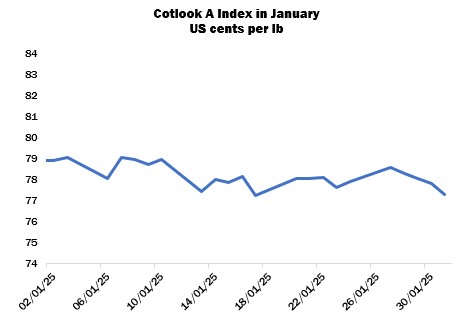

International cotton prices, as measured by the Cotlook A Index, declined by 160 points last month to be placed on January 31 at 77.30 cents per lb – its lowest value since November 16, 2020. The fall follows a similar trend in New York: the March contract lost 252 points overall, recording several new life-of-contract low closes, including on January 31 at 65.88 cents per lb. Market participants pondered whether a bottom had yet been found, or if prices had further to fall.

The weakness may be attributed in part to the substantial and persistent short position controlled by Managed Money investors that is yet to be covered. In addition, many other stocks and commodities markets also moved lower, perhaps in anticipation of the potential actions (including an array of promised tariffs) of the new US administration that took office in January, as well as in response to a swift fall in the value of several US Big Tech firms toward the end of the month. Fears of inflation in that country and beyond – which could be accelerated by tariffs and the potential responses from those countries targeted – as well as a stronger dollar also weighed on markets.

Import demand slowed somewhat in January, despite the bearish trend in prices, partly on account of the Lunar New Year holiday in many Southeast Asian countries. Meanwhile, basis levels for Brazilian and West African supplies in particular firmed perceptibly as trade long positions were depleted, which proved a further disincentive to mills. In addition, many buyers had already filled their cotton requirements for the coming months and some were concerned that lower prices in New York could in turn reduce the rates achievable for yarn below the cost of production.

Nonetheless, routine interest persisted from Pakistan, Bangladesh and Turkey, mostly for US and Brazilian lower grades or recaps, as well as the customary West African origins for Bangladesh. Some forward enquiry emanated particularly for Brazilian 2025 crop cotton, but reports of confirmed business were sporadic as mills’ price ideas were often below the level merchants were willing to contemplate. US export reports confirmed an acceleration in new commitments and shipments: weekly shipments recorded a marketing-year high in the period to January 9, while net sales registrations achieved the same feat in the week ending January 16.

Prior to the break, the lead contract on China’s Zhengzhou cotton futures platform firmed by 135 yuan, closing on January 27 at 13,640 yuan per tonne before trading was suspended for a week.

Ginning in Xinjiang reached 6.46 million tonnes before the holiday, just below Beijing Cotton Outlook’s forecast of output for the region (6,492,000 tonnes). The pace of ginning slowed, but work is expected to continue until mid-March. The China Cotton Association and Cncotton.com both raised their estimates of total production in January. Cotton Outlook’s own figure was increased by 100,000 tonnes to 6.9 million tonnes.

In the United States, the Department of Agriculture’s January review of estimates for 2024/25 included slightly higher domestic production and lower exports, resulting in ending stocks of 4.8 million bales, which would be the largest carryover since 2019/20 if realised. World ending stocks were also increased, by almost two million bales compared to the figure put forward in December, mostly as a result of larger crop estimates for China (up by 1.8 million bales from the previous estimate) and Australia (+400,000 bales) as well as the US (+160,000).

Field preparations got underway in the earliest sown areas of the US cotton belt, but more precipitation would be welcomed in many parts in the coming weeks and months to ensure sufficient soil moisture levels. A smaller planted area was still expected, although the size of the potential decline was debated among observers.

Seed cotton arrivals continued to dwindle in Pakistan: the Cotton Ginners’ Association reported the total at 5.51 million lint equivalent bales by January 31, up by just 58,500 bales from the end of December. Concerns were meanwhile raised regarding the lack of rainfall received so far, which could restrict irrigation for summer crops including cotton. Some early planting began in pockets of lower Sindh at the end of the month. In India, arrivals since October 1 reached 18.3 million bales by the end of January according to CCI. Auctions of the 2023/24 crop continued to be held by the Corporation, as well as procurement of this season’s supply.

In the Southern Hemisphere, heavy rains in Brazil’s producing state of Mato Grosso delayed the soybean harvest and therefore the sowing of safrinha cotton that follows. By January 24, just 29 percent of the intended area had been planted compared to 77 percent at the same date in 2024. Earlier in the month, the official forecasting agency CONAB increased its projection of cotton production in 2024/25 slightly to almost 3.7 million tonnes, as a result of higher figures for area and yields in northern growing regions. Ginning of the 2024 crop was essentially complete by the end of January. Export shipments achieved an all-time record for a single month in January of 415,000 tonnes.

Hot, dry conditions across the cotton belt in Argentina caused some plant stress, although the arrival of welcome rainfall provided relief in some fields. Many local assessments placed planted area at around 700,000 hectares nationwide and production expectations increased to more than 400,000 tonnes. In Australia, high temperatures also resulted in heat stress in certain fields, but here too scattered precipitation late in the month improved conditions in some areas. Overall, water availability was considered sufficient and production estimates for this season were circulating at above five million local bales. Grower selling was encouraged by the weakening of the Australian dollar versus the US currency, although forward sales of the 2025 crop remained modest.

In January, Cotton Outlook’s forecast of global raw cotton production in 2024/25 was increased by a further 333,000 tonnes, to 26.3 million tonnes. The rise is attributed to higher figures for Australia, China, India, the United States and others, only partially offset by reductions for Turkey and the African Franc Zone. Meanwhile, our consumption figure was left unchanged at 24.4 million tonnes. The margin by which production is estimated to exceed consumption in the current season has therefore increased to 1.87 million tonnes.