February 2025 Market Summary

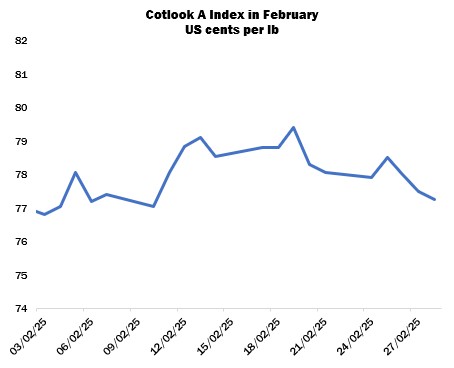

The Cotlook A Index moved in a range of less than three cents in February, ending the month barely altered at 77.25 cents per lb. In New York, however, the May delivery declined by 179 points overall, closing the month at 65.25 cents per lb, a contract low settlement. Market reaction to the release of potentially bullish supply and demand forecasts and US export reports (detailed below) was largely muted, and the negative trend was perhaps at odds with the relatively lively physical demand reported in several markets. The weakness may therefore be attributed at least in part to the significant short position held by Managed Money investors, which increased to 6.8 million bales by February 25, as well as the expectation of tariffs promised by the US and possible retaliation from the targeted trade partners.

Regular import demand was issued from several quarters during the month under review. Enquiry continued to be reported in Bangladesh for West African stocks, but trade inventories were depleted as replenishment at origin remained difficult on price grounds. Buyers in Vietnam, Turkey and Pakistan, as well as China, sourced mostly US and Brazilian supplies, including Brazilian 2025-crop for delivery later this year in the case of Pakistan. US cotton proved slightly easier to obtain following increased grower selling compared to other major origins, allowing a greater flow of business. Export reports confirmed the acceleration: new net sales registrations for the current marketing year totalled almost one million running bales during the month, while shipments recorded new marketing-year highs in three of the four reports covering February.

Meanwhile, the US Department of Agriculture left most figures for 2024/25 unchanged in its February domestic balance sheet, except for a modest reduction to domestic use, down to 1.7 million 480-lb bales, resulting in slightly higher ending stocks at 4.9 million bales. Adjustments to global estimates included higher production at 120.46 million bales, attributed mainly to an increase for China, as well as more modest rises for trade, consumption and beginning stocks, meaning that ending stocks are forecast half a million bales higher than the previous month at 78.41 million.

Looking ahead to the upcoming season, USDA published its first outlook for 2025/26 in late February. The area planted to all cotton in the US was placed in the report at 10.0 million acres, down from 11.2 million in 2024. Total production was forecast at 14.6 million bales, predicated on abandonment of 16 percent and yields of 833 lbs per acre.

The Department’s global estimates indicated that world cotton output in 2025/26 may be 3.8 million bales lower than the previous season, at 116.7 million bales, while consumption was forecast to rise by 3.1 million to 119.0 million bales.

In addition, the results of the US National Cotton Council’s Planting Intentions survey were released on February 16. According to the survey, which was concluded in January, the area planted to cotton beltwide in 2025/26 is forecast at 9.6 million acres, which would represent a 14.5-percent reduction from 2024/25 and the lowest area since 2015/16. The figure includes 9.4 million acres of upland and 27,000 of ELS cotton.

Upland area in Texas, the largest producing state, was placed at just over five million acres, down 16 percent on the year. In Georgia, a 22-percent decline is projected according to the survey, to 864,000 acres. Commentators noted that the forecast was perhaps slightly lower than anticipated, but recalled that last year’s initial figure from the Council was 9.8 million acres, 12.5 percent lower than the eventual outcome. The shift in farmers’ choices in 2024 was attributed in large part to the upward movement of the December ICE futures contract in the early weeks of the year, although no equivalent rise has occurred so far this season.

Elsewhere in the Northern Hemisphere, the Pakistan Cotton Ginners’ Association released its final report for the season, placing total arrivals at 5.52 million lint equivalent bales, around 34 percent lower than the Association’s figure for 2023/24, although a significant proportion of the crop is thought to have moved outside of official channels this year in order to avoid an 18-percent sales tax, and may therefore not be included in the PCGA figure. Early sowing of the 2025/26 crop progressed slowly, despite the Punjab provincial government setting an ambitious early planting target of one million acres in February and March. Some scattered showers were received during the month, but much more precipitation will be needed in the coming weeks following a drier than usual winter.

The Cotton Corporation of India placed cumulative arrivals since October 1 at 23 million lint equivalent bales by the end of February. Daily deliveries slowed to around 100,000 bales per day, and the Cotton Association of India reduced its output estimate for 2024/25, to 30.2 million bales.

In the Southern Hemisphere, sowing was complete in Brazil’s Mato Grosso state following delays owing to heavy rains that disrupted the soybean harvest, but observers commented that cotton planted outside of the ideal window will be more vulnerable to weather conditions in the coming weeks and months. Output estimates for 2025 by CONAB and ANEA converged at around 3.8 million tonnes. In Argentina, high temperatures persisted with isolated showers, but not enough to provide significant relief for dry fields. Groundwater table supplies in Chaco Province were close to or below historical minimal levels. Meanwhile, rainy conditions in Australia delayed picking in some areas and may have affected lint in open bolls.

Cotton Outlook’s initial forecasts for 2025/26 place global raw cotton production at 25.32 million tonnes (a decline of four percent from 2024/25), and consumption at 24.61 million tonnes (up by almost one percent). The result would be an additional rise of global stocks by the end of the next marketing year, of 711,000 tonnes.

Output estimates are lower in China and the US, with more modest falls envisaged elsewhere. Larger crops are meanwhile anticipated in Brazil, the Franc Zone and smaller producing countries. Meanwhile, the slight improvement projected for consumption is predicated on steady forecasts for global growth in 2025, as well as encouraging textile and ready-made garment export data from several markets. However, a degree of caution is necessary as we consider changing geopolitical events, tariffs and potential retaliatory actions, and the possibility of rising inflation and interest rates.