March 2025 Market Summary

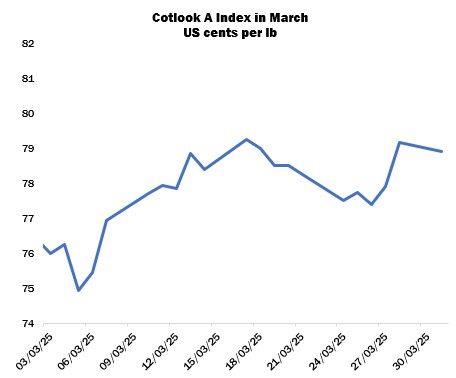

The Cotlook A Index declined early in the month, reaching its lowest level since October 2020 at 74.95 cents per lb on March 5, before recovering some ground to eventually end the period 165 cent points higher at 78.90 cents per lb. The rise followed a similar trend in New York: the May contract settled within a range of just over four cents, closing with a gain of 158 points.

These fluctuations, which were somewhat more volatile than those seen in recent months, were largely attributed to the changing trade policy of the US: tariffs on Chinese imports were raised from 10 to 20 percent on March 4, a move that was followed in Beijing with a 15-percent levy on US cotton imports starting on March 10. Then, Washington indicated that a new tariff agenda targeting various countries would be announced on April 2, again shaking confidence in financial and commodity markets as participants attempted to anticipate what might be included and the potential impacts on global trade, economic growth and inflation.

Import demand was of generally routine proportions in March, with activity slowing in Islamic markets in the approach to Eid. Nonetheless, buying was evident during price dips, but the focus remained on cotton available afloat or for nearby shipment rather than further ahead. Pakistan procured modest quantities of US and Brazilian cotton, often recaps, while those origins were also targeted by Vietnamese mills. West African supplies were as usual in demand in Bangladesh, but merchants’ holdings were low as the basis levels asked at origin were still too high for many trade buyers to contemplate. Brazilian 2024-crop supplies were also somewhat depleted, with roughly 93 percent estimated as committed according to IMEA (Mato Grosso’s economic institute), while 2025-crop sales reached around 60 percent of the anticipated final total.

Buyers in several destinations, then, continued to turn to US cotton to meet their requirements, albeit at a slower pace than observed last month. Export reports confirmed upland sales for dispatch this season of 586,300 running bales during March, below the 965,500 reported in February, while shipments remained robust at 1.54 million bales. Of note were the cancellations reported for China, largely accounting for a net reduction to that country’s upland commitment of 97,700 bales in March, as importers sought to avoid the retaliatory tariffs placed by Beijing on US cotton entering the country. Destination changes from China to other markets were also recorded, often to Vietnam. The latter country added 293,300 bales to its order book in March, 50 percent of the total increase reported for all destinations.

The lead delivery on China’s Zhengzhou cotton futures platform ended the month modestly lower, at 13,545 yuan per tonne. Inspections of the 2024/25 crop in Xinjiang reached 6.66 million tonnes by the end of March, while new crop sowing expanded in southern Xinjiang, to be followed by northern areas in April.

Meanwhile, the USDA’s Prospective Plantings report was published on March 31, indicating expectations of a total planted area in the US for 2025/26 of 9.87 million acres, well within the range of estimates circulating before the report’s release. However, observers noted that 60 percent of the expected area is in Texas and Oklahoma, where weather conditions are especially crucial in determining final output (average abandonment levels over the past five years amount to 47 and 41 percent, respectively). In March, though, many fields in those states were experiencing severe drought and growers noted that rains were urgently needed as sowing begins.

In its monthly supply and demand assessment, USDA left its domestic 2024/25 figures unchanged, including production at 14.4 million 480-lb bales, exports at 11.0 million and ending stocks at 4.9 million. Its world estimates, though, were subject to modest revisions. Global output was increased slightly to almost 121 million bales, while consumption was increased to 116.5 million, with the result that ending stocks were adjusted downward to 78.3 million.

Elsewhere in the Northern Hemisphere, 2025/26-crop planting expanded in the earliest sown areas of Pakistan, aided by warm weather. However, water shortages hindered work in Sindh in particular, and growers indicated that planted area could be lower than intended if water availability does not improve in the coming weeks.

Meanwhile, the Cotton Corporation of India placed cumulative arrivals since October 1 at just over 26 million lint equivalent bales by the end of March, up from 23 million by the end of February. Various bodies in the country reduced their production estimates for the season, to around 29.5 million local weight bales, although many observers held slightly more optimistic views. CCI also began auctions of 2024/25-crop cotton early in the month with relatively muted participation at first, but sales began to pick up pace in the latter half of March.

In the Southern Hemisphere, heavy precipitation was received in Brazil’s Mato Grosso state, disrupting pesticide applications, with the result that some infestations were reported. Helpful scattered rains were received in Bahia, but many fields remained drier than would be ideal. Some local output estimates were revised downwards. In Argentina, dry conditions persisted, and growers noted severe damage to crops and losses in many fields. Some precipitation was received later in the month, but was thought to have arrived too late to benefit most stands. A tropical cyclone made landfall on Australia’s east coast in early March, bringing damaging winds and heavy rains to coastal areas and lighter precipitation to cotton fields. Warm, dry weather followed, allowing open bolls to dry out but another weather system arrived as the month came to an end, bringing additional widespread rains as picking was poised to expand in many fields, leading to concerns that the grade composition of the crop could be affected.

Cotton Outlook’s estimate of world raw cotton output in 2024/25 was reduced by 256,000 tonnes in March, to 26.08 million. Lower figures for India, the African Franc Zone and others were partially offset by increases for China and Australia. A more modest downward adjustment was made for 2025/26.

Our consumption estimates were meanwhile raised for both the current and upcoming seasons, by 391,000 and 325,000 tonnes, respectively. Therefore, global stocks are expected to rise by 1,225,000 tonnes by the end of 2024/25, and 366,000 tonnes by July 31, 2026.