February 2024 Market Summary

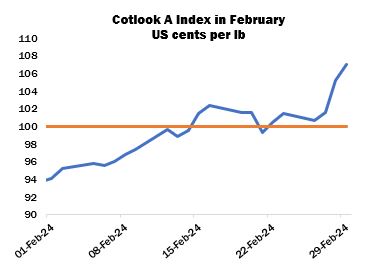

In stark contrast to much of last year, volatility characterised the ICE futures market in February. The upward trajectory that began the previous month, as speculators reacted to the tightening US balance sheet, continued and several strong rallies were observed. By the end of the month, the May contract had crossed the dollar threshold. The net gain during the period was more than 13 cents. Turnover continued to be heavy. The July/December spread had meanwhile widened to 1,400 cent points (July premium) by February 29. Prices in the physical market followed the lead of New York: the Cotlook A Index was placed on the first day of the month at 94.1 cents per lb and on the last day at 107.0 cents per lb (also the high for February), and was above the dollar mark for a total of ten days.

The Lunar New Year holiday paused trading in China between February 9 and 19. Upon return, the Zhengzhou cotton futures market reacted in rather muted fashion to the rallies in New York, advancing slightly in the first session before falling back and remaining in a relatively narrow range thereafter. The May contract closed at 16,200 yuan per tonne on February 29, with a net gain on the month of 155 yuan, a fraction of the rise in New York. Local spinners were still encountering slow demand from the downstream textile sectors. Meanwhile, supplies from the domestic 2023/24 crop were abundant, as were consignments of imported cotton that continued to arrive at Qingdao and other ports.

In other markets, mill demand retreated as a result of the firmer prices and volatility, although some spinners took the opportunity to execute their earlier higher priced contracts. The slower pace of yarn price rises also served to inhibit enquiries other than from a few mills with urgent requirements to cover. The focus of the latter was frequently on cheaper lots and those discounted on quality grounds. Selling from origin was also observed, including via tenders in West Africa.

Lower basis levels for Indian cotton relative to New York prompted fresh business both in the local market and for export. However, erratic price movements later in the month somewhat dampened demand. Buyers in Bangladesh, though, continued to favour the neighbouring origin on both price and logistical grounds. The Indian government removed an 11-percent import duty on long staple cotton, effective from February 20, although that for upland styles remained in place.

Attention steadily turned to the prospects for the 2024/25 cotton crops in the Northern Hemisphere. In the United States, first estimates of next season’s planted acreage were published by the Department of Agriculture and the National Cotton Council. The USDA forecasted cotton plantings at 11 million acres, representing an increase of 7.5 percent from the previous year, and output at 16 million bales, up 29 percent. Conversely, the National Cotton Council placed planted area at 9.8 million acres, which would represent a decline of 3.7 percent from 2023/24. It was acknowledged, however, that the Council’s figure was based on grower surveys conducted in December and January when ICE futures were at lower levels than in February, and that an acreage number closer to the USDA’s estimate could be in prospect.

Elsewhere in the Northern Hemisphere, the Cotton Corporation of India placed domestic seed cotton arrivals from the current crop at 21.4 million bales by the end of the month, more than two thirds of estimated output. Deliveries were partially disrupted in the Northern Zone as a result of farmer protests, while some growers across the country held back supplies in hopes of taking advantage of the rising trend in local prices.

In Pakistan, early cotton planting began in a few areas, despite cooler than ideal temperatures. Growers are encouraged by the potential for better yields as the risks of pest attacks and damage by Monsoon rains appear less severe for those plants sown and harvested earlier than others. Firmer local lint prices since the turn of the year may also provide a positive impetus for cotton growing in the next season. According to the Cotton Ginners’ Association, seed cotton arrivals from the 2023/24 crop by February 29 stood at 8.39 million lint equivalent bales, which may well be the final figure for the season.

Turning to the Southern Hemisphere, sowing in Brazil was essentially complete by the end of February and young plants were said to be progressing well in both of the main producing states. CONAB placed its official crop forecast at just below 3.3 million tonnes, which would be a record output. Some early harvesting began in Argentina, albeit at a slow pace as the peak picking season remains some way off. Rains were received to the benefit of still developing plants. In Australia, hot and humid conditions persisted while optimism was largely maintained for another bumper crop of over one million tonnes.

Cotton Outlook’s initial estimates for the 2024/25 season, published as usual at the end of February, placed world raw cotton production at 24.9 million tonnes, indicating an increase of 1.8 percent on the current season. The single largest rise was forecast for the United States, largely attributed to expectations of better yields and lower abandonment in Texas. Global consumption was meanwhile forecast to rise by three percent, to 24.5 million tonnes. Thus, the result would be an addition to world stocks by the end of the next marketing year, of 435,000 tonnes.